Report Overview:

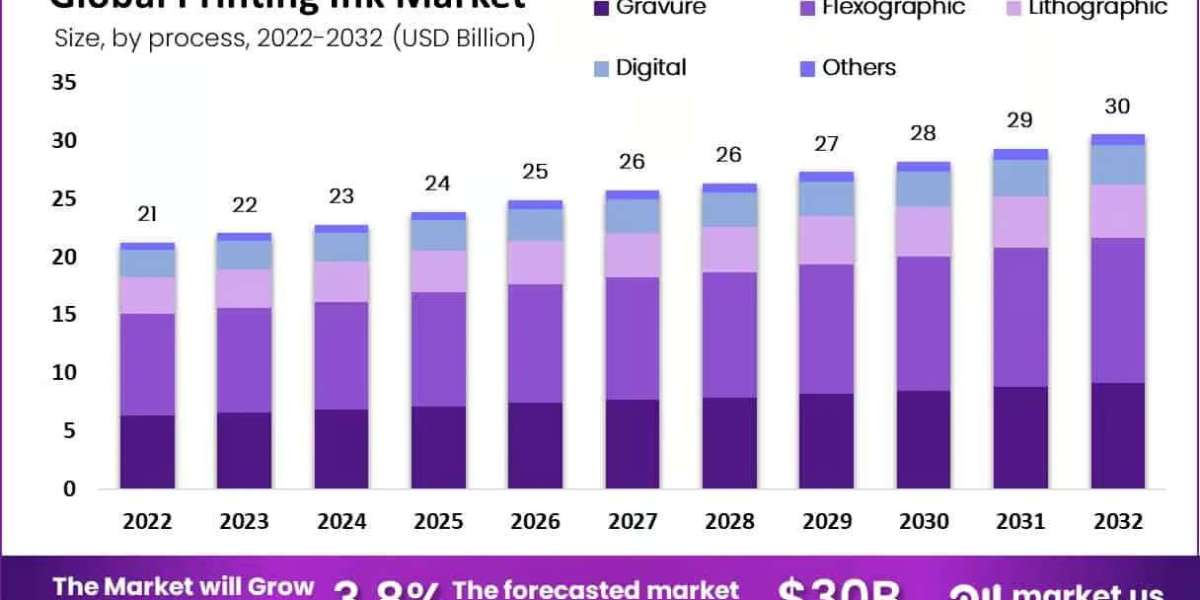

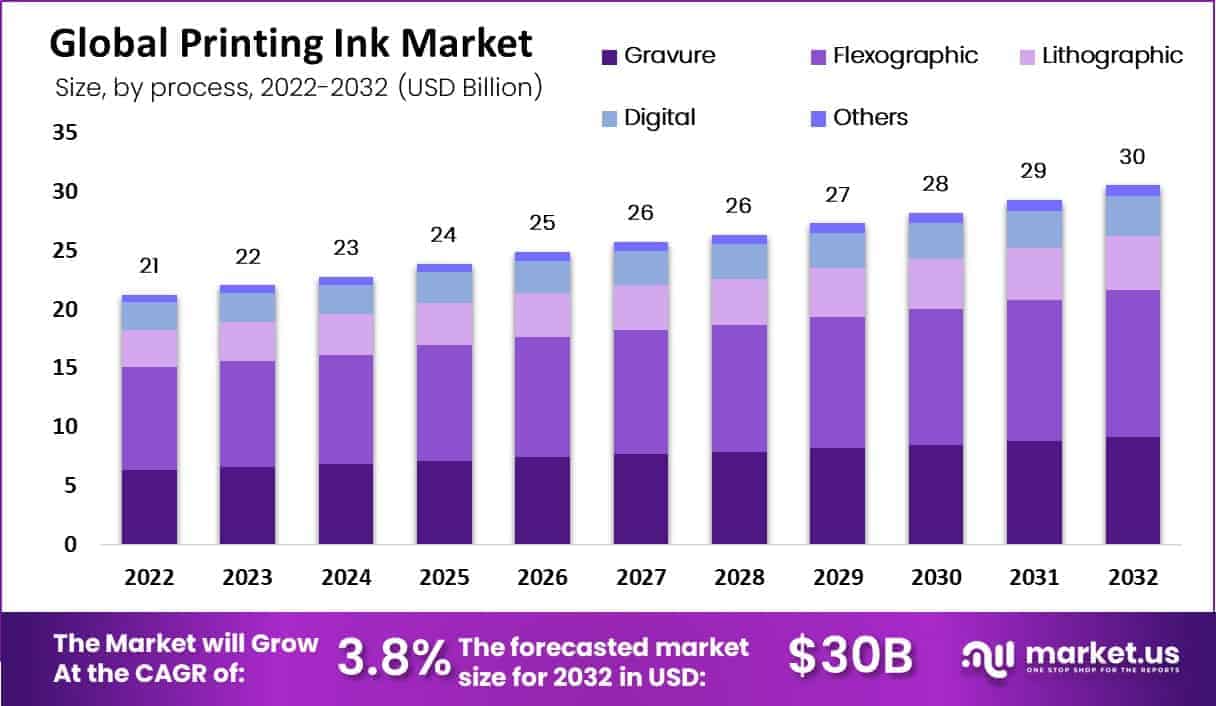

In 2022, the global printing ink market was valued at approximately USD 21.2 billion. It is projected to reach around USD 30 billion by 2032, growing at a compound annual growth rate (CAGR) of 3.8% over the forecast period from 2023 to 2032.

Printing inks made from pigments or dyes mixed with carriers such as oil, water, or solvents play a vital role in packaging, commercial printing, and specialty applications. Growth is primarily driven by strong demand from packaging and labeling sectors, particularly in the food and beverage industry. Asia-Pacific leads the global market, holding approximately 38% revenue share in 2022, supported by expanding industrial activity, e-commerce, and modern packaging requirements. Meanwhile, water-based and UV-curable inks are gaining traction due to environmental regulations and consumer preferences, although traditional oil-based inks continue to hold significant market share.

Key Takeaways:

- Market Size and Growth Projection: The printing ink market was valued at USD 21.2 billion in 2022. It is expected to grow to approximately USD 30 billion by 2032. The market is projected to register a Compound Annual Growth Rate (CAGR) of 3.8% between 2023 and 2032.

- Printing Ink Composition: Printing inks are used for creating images, text, and designs, and they contain dyes or pigments. They are commonly used in lithographic and letterpress printing. Inks are made by mixing pigments of the desired color with varnish or oil.

- Types of Printing Inks: Carbon black is often mixed with linseed oil or similar oils for traditional printing inks. Inkjet inks are composed of a base carrier (water, oil, or solvent), colorants (dyes or pigments), and chemical additives for special qualities.

- Regional Market Analysis: Asia Pacific held the highest revenue share (38.0%) in the printing ink market in 2022. Market growth is positively impacted by the consumption of packaged food items and the labeling industry in the region.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/printing-ink-market/free-sample/

Key Market Segments:

Based on Process

- Gravure

- Flexographic

- Lithographic

- Digital

- Others

Based on Formulation

- Oil Based

- Solvent Based

- Water Based

- UV- Cured Based

Based on End-User

- Packaging

- Commercial Publication

- Textiles

- Other End-User

Drivers

One of the key forces driving the global printing ink market is the rapid growth in packaging and labeling, particularly in sectors like food, beverages, pharmaceuticals, and personal care. Brands are investing heavily in eye-catching and functional packaging that communicates product details clearly while also standing out on shelves. This has directly led to increased consumption of various printing inks that support high-quality, durable, and colorful print work. Another critical driver is the demand for environmentally compliant solutions.

Packaging and labeling remain the largest drivers of ink demand as consumer-facing brands emphasize vibrant, protective, and informative printing. Regulatory pressure for low-VOC products fuels the uptake of water-based and UV-curable inks, aligning with environmental goals. Meanwhile, digital printing technologies are allowing shorter print runs and greater customization, adding to ink consumption for commercial and direct-mail applications.

Governments and organizations across the globe are pushing for lower volatile organic compound (VOC) emissions. As a result, water-based and UV-curable inks known for their eco-friendly composition and performance are gaining popularity across industries. Furthermore, the growth of digital printing technologies has also added momentum. These technologies support short-run and customized print jobs, which are ideal for personalized marketing campaigns, product testing, or localized packaging. Digital printing’s flexibility and speed have made it an integral part of the evolving print ecosystem, thereby increasing the demand for compatible ink formulations.

Restraining Factors

Despite the positive outlook, the market faces several constraints, especially related to raw material cost volatility. Printing inks rely heavily on petrochemical-derived components such as resins and solvents. Fluctuations in oil prices and supply chain disruptions can make production planning difficult and squeeze profit margins particularly for smaller and mid-sized ink manufacturers.

Regulatory pressure is another major challenge. Several jurisdictions, especially in North America and Europe, impose strict limits on the use of VOCs, heavy metals, and other hazardous substances in inks. Adhering to these regulations requires ongoing investment in reformulation and R&D, adding both time and cost burdens. There is also the broader challenge of digital disruption. As digital media consumption continues to rise, the traditional print segments such as newspapers, magazines, and brochures have seen declines. This shift has forced ink manufacturers to refocus on packaging and other resilient application areas. Meanwhile, short-run printing demands challenge the economies of scale that conventional ink production once relied on.

The market faces cost pressure from volatile raw material prices, especially for solvents and resin components. Environmental regulations, particularly on VOCs and heavy metals, add compliance complexity and R&D costs. Traditional print still competes with digital media and packaging shifts, creating resistance in legacy segments. Short-run customization also challenges large-batch ink producers.

Opportunities

As the industry evolves, sustainability opens up one of the most promising growth opportunities. There's rising interest in bio-based pigments and low-VOC inks, especially among environmentally aware consumers and in regions with stringent regulations. These products not only meet compliance standards but also align with brand values focused on environmental responsibility.Specialty inks present another fast-growing opportunity.

From conductive inks used in printed electronics to antimicrobial inks in healthcare packaging and heat-sensitive formulations for smart packaging, innovation is expanding the range of applications for printing inks. As technology advances, these high-value inks will play a larger role in differentiating brands and enhancing product functionality. Additionally, emerging economies in Asia-Pacific, Latin America, and parts of Africa are experiencing strong retail and e-commerce growth. As disposable incomes rise, so does the demand for packaged goods driving up ink consumption for packaging and labeling. Coupled with ongoing infrastructure development, these regions offer a significant runway for expansion.

Sustainability offers a major opening bio-based pigments, waterless printing, and low-VOC systems appeal to eco-conscious buyers and regulatory bodies. Specialty inks such as conductive, antimicrobial, or heat-sensitive formulations are gaining traction in electronics, healthcare, and smart packaging. Growth in emerging markets with rising disposable incomes and retail expansion presents another key opportunity. Additionally, the shift to personalized and premium packaging drives demand for advanced ink formulations.

Trends

The printing ink market is undergoing a transformation led by innovation, regulation, and shifting end-user needs. One of the strongest trends is the widespread adoption of water-based and UV-curable inks. These alternatives not only reduce environmental impact but also offer excellent durability, faster drying times, and improved adhesion across diverse surfaces. Flexographic printing, which heavily uses water-based inks, is increasingly used in food and corrugated packaging due to its eco-friendly nature and high efficiency.

As the demand for recyclable and compostable packaging grows, flexographic and digital printing are taking center stage. Another major trend is the rise of digital and on-demand printing, which allows for personalization, localized campaigns, and efficient inventory management. This is especially relevant in sectors like cosmetics and beverage labeling, where agility is key. Lastly, Asia-Pacific remains a dominant force in this industry, fueled by manufacturing growth, urbanization, and expanding middle-class populations. Developed markets, meanwhile, are leaning into premium, sustainable, and smart packaging solutions as part of the evolving consumer experience.

Water-based and UV-curable inks continue to grow, supported by regulations and performance benefits like quick curing and durability. Flexographic printing, which uses such inks, is expanding in food and corrugated packaging. Digital and on-demand printing are reshaping market dynamics, with specialty inks tailored to niche industrial needs. Asia-Pacific remains the primary growth region, while mature markets pivot toward eco-sensitive and smart-label technologies.

Market Key Players:

- DIC Corporation

- Flint Group

- Toyo Ink SC HOLDINGS CO., LTD.

- Huber Group Deutschland GmbH

- SAKATA INX CORPORATION

- ALTANA AG

- Wikoff Color Corporation

- Sun Chemical

- Tokyo Printing Ink MFG CO., LTD

- Other Key Players

Conclusion

The printing ink market is growing steadily, primarily driven by packaging and labeling demand and the rise of eco-friendly formulations. The shift towards sustainable ink types such as water-based and UV-curable aligns with global environmental policies and customer preferences. As Asia-Pacific leads expansion, brand packaging and e-commerce demand play central roles.

Digital and flexible print technologies further diversify the market by enabling customization and premium print offerings. Looking ahead, innovation in sustainable pigments, specialty formulations, and smart inks will define success. Manufacturers must balance regulatory compliance with cost-effective, high-performance products. With careful investment in R&D and a focus on emerging regions, the printing ink market is well-positioned to grow toward USD 30 billion by 2032 offering reliable, vibrant printed solutions for industries worldwide.